Hi all, since starting this newsletter about my own portfolio in June, I have never gotten enough time to write. My apologies! A whole quarter has elapsed since then, so I absolutely need to write something now.

Back in June, I wanted to write a report on $DIDIY, a high-conviction position that is currently the third-largest single-entity position in my portfolio, accounting for ~7% at the moment. I will try to finish the write-up, but first, I realize I should provide a brief overview of my overall portfolio before proceeding.

As of the day of writing this article, September 28, 2025, my portfolio’s NAV/unit stands at $6.7365, representing a quarter-on-quarter return of 15.3% compared to when I disclosed it at the end of June. This return is to be expected, given the China-heavy nature of my portfolio and the current bull run in the China equity space. (For my overall assessment of the long-term durability of this bull, please read here.)

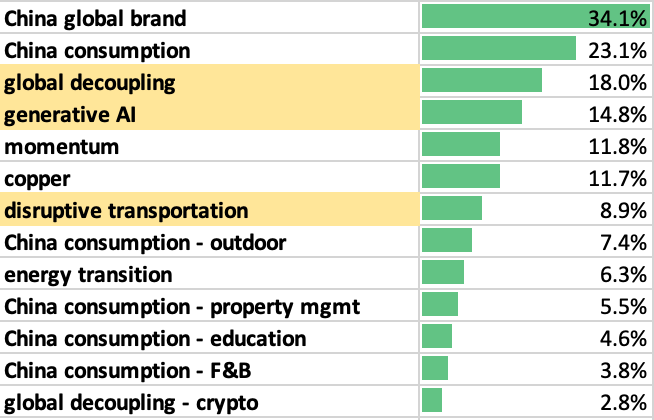

Themes

I wrote last time that my portfolio followed a thematic-driven and sector-driven approach. Below are all the themes and their respective current portfolio weights.

Please note that these themes are not mutually exclusive. For example, almost all the positions under “China global brand” are categorized by other themes as well, while “China consumption” encompasses a range of smaller sub-themes, including outdoor, property management, and others.

The three themes highlighted in yellow at the moment are the areas I am currently paying special attention to, and I may expand on them should circumstances allow.

I will briefly explain these themes one by one.

China Consumption

I would like to begin with the second-largest, “China consumption”, which accounts for 23.1% of the portfolio. I believe that for all retail investors, consumption should always be a major component of any portfolio. Consumption is where regular retail investors can be expected to have a special edge. Because, after all, every one of us is a consumer in some way. The intuitive understanding of a product's strengths and weaknesses may already put you ahead of the curve, compared to fund managers who have never had personal experience.

I also hold the strong view that China’s consumption will enter a prolonged cycle. We have talked about this many times at Baiguan. In short, a historic pivot from over-production to a more balanced relationship between consumption and production is undoubtedly underway, and has become a social and political consensus in China.

My “China consumption” portfolio is primarily comprised of four major sub-portfolios: outdoor spending, property management services, after-school education, and food & beverages. All of these four areas either have highly defensible business models, and/or potential for outsized growth. I will elaborate on these in Part 2.

Global decoupling

Great global decoupling and mutual distrust among nations is a given fact in our time and is going to last in the foreseeable future. Many of the best-performing asset classes in the last few years are directly related to this fact.

Around 12% in my 18% decoupling position is in copper-related positions (I will elaborate on this in Part 2), and around 7% is gold-related. Gold and copper are often related (they are often mined together), so there is an overlap here, mainly in the form of my holding of Zijin Mining (2899.HK), which is a major mining conglomerate of both gold and copper.

I see crypto as a direct beneficiary of this decoupling, too. If our world functions as if it were a “global village”, headed by a hegemon and shaped by the same rules and aspirations, then the opportunities for crypto will at best be peripheral. But we are not in that world. Instead, we live in a world that has become both multipolar and chaotic, where every nation prioritizes its own interests and is increasingly skeptical of others. In such a world, crypto, a technology designed for a “trustless” environment, has an essential role to play.

Crypto-related equity positions account for a little below 3% of this stock portfolio, and are mostly made up of crypto ETFs such as IBIT 0.00%↑ and ETHA 0.00%↑. However, my actual conviction in crypto is much higher than that. I have been regularly investing in Bitcoins since 2016 and maintain a separate portfolio from my stock portfolio. Bitcoins made up a substantial portion of my entire investable assets, primarily due to the exploding value in the last decade and the fact that I almost never sold them. For this newsletter, I will exclude my direct crypto holdings.

Another major way for me to play global decoupling is to invest in countries that can become net beneficiaries of the decoupling, especially the US-China decoupling. For this, I have long-term positions in country ETFs on Vietnam ($VNM), Mexico ($EWW), Japan ($EWJ), and India (for India, I only invest in INCO 0.00%↑ a consumer index). These country ETFs make up a little less than 3% of the total portfolio.

Generative AI

I have conflicting feelings about generative AI. On the one hand, there is no doubt that GenAI technologies are our era’s revolutionary technology. For knowledge-hungry people like me, AI has been a great companion in searching for information and knowledge, and has been an untiring assistant on tasks that are both mundane and necessary, such as filling out a pointless form. For me, AI has liberated a great amount of my productivity, and I have paid at least hundreds of dollars a year for different applications already.

On the other hand, I can’t shake off the feeling that, despite the amount of productivity it has unleashed, it won’t provide adequate returns on the kind of astronomical capital expenditures that are slated to be spent on it. My key thesis, which I may expand on one day, is that only a tiny fraction of the entire population, comprising knowledge workers, will find AI based on large language models to be useful. However, two cognitive errors lead most people to believe that trillions of capital expenditures are worthwhile.

First, all capital and media are controlled by knowledge workers as well. We love this technology so much that we grossly overestimate its real-world impact. Second, we implicitly assume that because AI has advanced so fast, robotics will be coming soon. General robotics will truly unleash the kind of productivity that industrial revolutions did in the past. But robotics has nothing to do with languages. It’s just plain wrong to assume we are close to the “ChatGPT moment” in robotics.

Because of these cognitive errors, I believe we have already entered a perilous bubble territory, a bubble that could potentially crash the entire market into a dot-com-type disaster. But since we don’t know when the music will stop, we can still keep dancing.

It was my mistake to fail to capture the spectacular growth of NVDA 0.00%↑ back in 2023, when I should have invested heavily in it. The writing on that wall was crystal clear. As of late 2025, due to the aforementioned doubts, my overall AI-related positions are not substantial, accounting for only ~15% of the portfolio. Compared to the outsized hype this sector is currently enjoying, I consider this to be an underweight position.

And my picks for this sector are “conservative” too. A great majority, which is ~9% of this 15%, is Tencent, my second-largest holding and a position that I have held for many years. Without Tencent, my “Gen AI” holding would be as meager as only 6%.

I have only recently classified Tencent as “Gen AI” because, overall, I see content businesses as the primary beneficiaries of this wave of generative AI. After all, generative AI is great at generating content, which leads to even stickier user engagement. For the same reason, I will look for opportunities to invest in Bytedance/Douyin if they ever get listed.

The other strong beneficiary of the AI age is the owner of proprietary data assets. Large language models, after consuming all of the data in the public domain, will tap into proprietary and high-quality data to stay differentiated. For this reason, I have a ~2% position of RDDT 0.00%↑ before I got more time to research this topic. Recently, it has surged to levels that I couldn’t really comprehend. I wish I could buy more!

For this same reason, I will also keep an eye on stocks such as NYT 0.00%↑, SPGI 0.00%↑, MSCI 0.00%↑, NIQ 0.00%↑, etc. My favorite on that watchlist, though, will be Substack itself. I believe this one will become a major repository of high-quality human knowledge in the age of AI. So,

and , I wish you guys a successful IPO soon, because I will be dying to invest.My other holdings are MSFT 0.00%↑, GOOG 0.00%↑, and BABA 0.00%↑, the latter two of which I only added for opportunistic reasons within the last quarter.

However, overall, I am more cautious than optimistic, for the aforementioned reason that the people who are harping on AI today are too loud, and the actual impact of this AI on the broader economy remains elusive. I believe it will become truly impactful one day, just like the dot-com crash eventually led to a new era of mankind and some of the most valuable companies in history. But that only happened after many years of post-crash despair. I just can’t see that coming in a year or two.

Momentum

Sometimes I invest not just because the underlying business has high quality, but I also invest to purely ride the wave of market sentiment. This is the “fun” part of my portfolio, and I have no shame about that.

A regular attendee in this segment is FUTU 0.00%↑, Greater China’s largest retail broker, and China’s Interactive Brokers + Charles Schwab + and Robinhood. This is a great company, managed by a great team, whose product I have used and enjoyed for more than a decade.

Yet at the same time, because it is a broker, it’s also a high-beta play, which means you will always have the opportunity to buy at an extreme low and sell at an extreme high. Looking at its price chart for the last 5 years, you will know what I mean:

Because of these traits, FUTU 0.00%↑ has been the largest contributor to my returns in history. The historical returns because of it account for at least 25% of my portfolio, and despite my selling most of my positions in it back in 2021 at the height of market craze, it has still surged to become my single largest position recently, at almost 10%.

Other smaller momentum-driven positions include Value Partners (806.HK), a major Hong Kong fund manager, some leveraged ETFs like CHAU 0.00%↑ and YINN 0.00%↑, and some stock options. These are just for fun.

Part 2, due to be published during China’s Golden Week holiday (Oct 1 - Oct 8), will touch on my other key themes, including:

Why I have a high long-term conviction on copper

My view on “disruptive transportation”, my catch-all phrase for the AV/EV space

Why is my enthusiasm for green energy not high, and for robotics, non-existent

Several key sub-themes of “China consumption”, including outdoor activities, property management, after-school education, and food & beverages

How I play the “go global” trend of Chinese brands

Disclaimer: It is highly recommended that you read about my investment style to understand my numerous limitations. The information contained in this newsletter is for informational purposes only and should not be construed as financial, investment, or other professional advice. I am not a licensed financial advisor, and nothing here constitutes a recommendation to buy, sell, or hold any securities. Investing in financial markets involves risk, including the possible loss of principal. You should conduct your own research and consult with a qualified financial professional before making any investment decisions.

Great read!