EV, autonomous driving, robotics, new energy, China consumption & Chinese brands going global

2025Q3 Portfolio Review (Part 3)

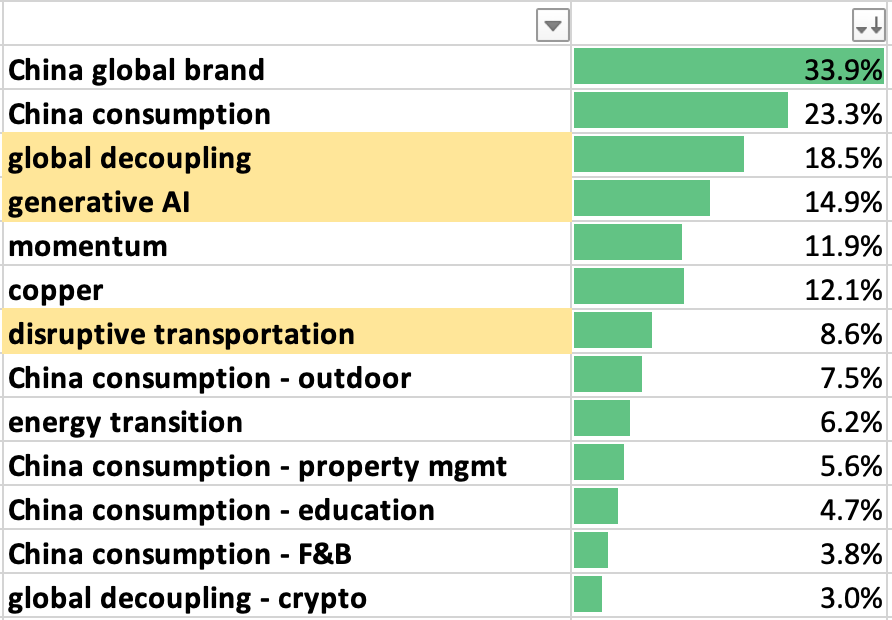

In Part 1, I gave you the rough overview of the themes in my portfolio, and how I see China consumption, global decoupling, and generative AI as my top themes. In Part 2, I specifically discussed my long-term conviction in copper.

In Part 3, I will finish the review for this quarter, including:

My view on “disruptive transportation”, my catch-all phrase for the AV/EV space

Why is my enthusiasm for green energy not high, and for robotics, non-existent

Several key sub-themes of “China consumption”, including outdoor activities, property management, after-school education, and food & beverages

How I play the “go global” trend of Chinese brands

Disruptive transportation

Another significant theme I am watching and waiting for is the historic disruption in transportation, in the form of both electrification and autonomous driving.

The story of electrification is well-established. I used to hold significant shares of both BYD (1211.HK) and CATL (3750.HK), but I have sold most of them this year. In the case of BYD, I am concerned that electric vehicles have entered a stage of commoditization, and the competition is simply too intense to make me sleep comfortably at night. While in the case of CATL, although it’s in a better market position in batteries than BYD in EVs, the valuation level (and the ~40% premium over its A shares) makes me uncomfortable. After all, selling batteries should even be more commoditized than selling cars. And if I want to invest in commodities, I have found the perfect commodity to play electricification, so why bother?

The story of autonomous driving/robotaxi is far less established, but holds a greater promise. And it’s not a fairy tale technology anymore. Experiments by Waymo, Tesla, and even Baidu have shown that robotaxi services can not only be technically feasible but also have the potential to be commercially viable at scale. It is possible that we are on the eve of mass adoption.

For this theme, I hold tiny positions of TSLA 0.00%↑, PONY 0.00%↑, WRD 0.00%↑, just to remind myself that I should pay attention to them and keep learning. My highest conviction, though, which is right now 7% of my entire portfolio, is Didi. I will explain my thesis in a separate article soon.

What about robotics? Unlike autonomous driving, I don’t think we are at the eve of a revolution of general robotics at all. The success of large language models gives many people the illusion that we are close to general intelligence in the physical world as well. This is not true. The world of languages and symbols, on which the LLMs are built, is entirely different from the world of physical agility. And the fact that robots can do a crazy dance with pre-programmed algorithms tells us nothing about how far we are away from having robots that can do undefined types of housework for us.

With so much training and data, humanity has yet to achieve a “perfect” autonomous driving system. Otherwise, adoption of the technology should be a no-brainer decision for consumers. But apparently, because our current autonomous driving technology is barely “good enough”, it’s not a no-brainer.

And driving should be considered “easy”. It has clear rules: moving between two lanes, from point A to point B. So even with this “easy” task, we struggle, and even if we are to perfect it one day, it would only be the “AlphaGo moment” in robotics: having a near-perfect system in an ideal, pre-defined environment, but we will still be far away from achieving a “ChatGPT moment” in robotics.

So don’t tell me we are going to achieve a general robotics system that can deal with all tasks, in all terrains, in 1 year, or 3 years, or even 5 years. I won’t buy into this hype, for now. But I will keep a close watch just on autonomous driving.

Energy transition

I believe that by the second half of our century, green energy will be the dominant source of energy. This is not just due to climate concerns, but the majority of the world, especially developing countries, would want to wean themselves off fossil fuels, if only for national security concerns. This natural urge, coupled with the ability of China to deliver the means, would make this transition but a sure thing.

Yet, despite such a dramatic and historic change, this theme is still only at around 6% of the portfolio, and I don’t wish to add more in the near future. I have struggled to invest in this sector, given that much of it, from solar panels to batteries, is easily commoditized and extremely cyclical. In fact, we, inhabitants of the earth, actually “want” it to be as commoditized as possible, since only cheap green energy can lead to mass adoption. So I just can’t see a defensible business moat here.

And even the paltry 6% is ironically mostly invested in traditional fossil fuels, such as CNOOC (883.HK). A distaste for fossil fuels leads to a lack of investment in traditional oil and gas projects, which means lower competition and more stable margins for the incumbents.

Sub-themes within “China Consumption”

For my general take on China’s consumption, please refer here.

Outdoor spending

A big structural shift in Chinese people’s spending behaviors is that, compared with the past, we are spending more and more time outdoors. This is a trend that will benefit sectors ranging from outdoor sports to tourism. I have about 7.5% of my portfolio covering this theme, mostly including positions in tourism (TCOM 0.00%↑, HTHT 0.00%↑, ATAT 0.00%↑) and sportswear (Anta (2020.HK), AS 0.00%↑.) I am also keeping a small position in an outdoor vehicle specialist, called Vala (2051.HK), and have been following it intently.

Property management services

Property management is a niche sector that I have been following for many years. My top positions are Greentown Services (2869.HK) and Onewo (2602.HK). It’s a sector with unique Chinese characteristics, secular growth potential, but also long-term worries. I will write about this sector in a separate note.

After-school tutoring

I have very conflicting feelings about this sector. I captured part of this sector’s rebound from the depths of the government crackdown, but I used to hold twice as many as I currently hold. To my knowledge, this sector (made up of mainly two players) can no longer be characterized as a high-growth sector. But the valuation, at EV/FCF of single digits while also buying back their own shares aggressively, can be a great cigarette butt type of investment.

Food & beverages

Chinese people love food. For this, I hold YUMC 0.00%↑, Luckin Coffee, and keep a tiny position in CHA 0.00%↑, just to keep an eye out. And I have a lot more on my watchlist.

Chinese brands going global

This represents a significant growth delta of our era. This is what I firmly believe in.

Over the past decades, China has dominated the world’s manufacturing capacity. But in the realm of brands and narratives, China still lags significantly behind top American and European firms. All the “high-culture” sectors, ranging from luxury to the information services industry that I work in, would be the last “stronghold” to crack open for Chinese businesses.

And we are already seeing early signs. The best case in the last few years is the global success of POP Mart, a spectacular story that I unfortunately never invested in and probably never will, as I still don’t understand its appeal to this day. (But my colleagues at Baiguan unearthed its story long before it reached consensus.)

POP Mart is definitely not alone. Black Myth: Wukong proved that Chinese teams are able to produce top-of-class video game content.

I believe these are not isolated cases, but would be the most exciting theme for the next 2 decades. There is no clear way to play this theme, but it serves as a general reminder that I should go after the names that have the potential for global appeal. My positions in Tencent, Futu, Didi, and Luckin all have untapped potential in this regard, and I am hoping to find more!

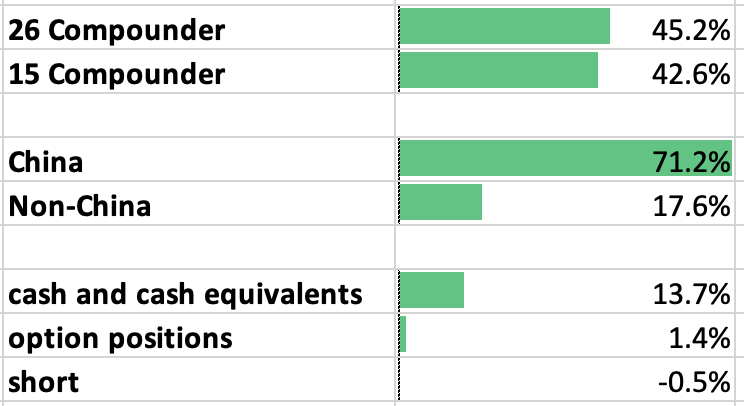

For your reference, this is the composition of my portfolio as of Sep 30, 2025, pre-US trading time:

By themes (mutually non-exclusive)

By types (definition)

Top 20 positions

Disclaimer: It is highly recommended that you read about my investment style to understand my numerous limitations. The information contained in this newsletter is for informational purposes only and should not be construed as financial, investment, or other professional advice. I am not a licensed financial advisor, and the information provided here does not constitute a recommendation to buy, sell, or hold any securities. Investing in financial markets involves risk, including the possible loss of principal. You should conduct your own research and consult with a qualified financial professional before making any investment decisions.

Interesting set of themes. Thanks a lot for sharing and the copper view as well! Could you expand in a future article on FUTU, Tencent and Didi?